Should the employee stock purchase program deserve more attention? Is it a viable strategy for attracting and retaining top talent in your organization? Find out in this article

- The basics of stock purchasing plans for employees

- How an employee stock purchase program works

- Typical employee eligibility requirements to purchase stock

- Types of employee stock purchase programs

- How employees pay taxes on an employee stock purchase program

- What happens to an ESPP when an employee leaves?

- Should your company really set up a stock purchasing program?

Employee benefits play a major role in attracting and retaining top talent. If companies or organizations wish to attract high-performing employees and keep them, the benefits they offer must likewise be of a high calibre.

One type of employee benefit that has enjoyed great popularity and success across industries is the employee stock purchase program (ESPP). This is a benefits program that allows employees to buy into their own company’s stock and reap the benefits when it increases in value.

Apart from motivating employees with monetary benefits, an ESPP can also do good for a company’s efforts to achieve its long-term corporate goals. In this guide, Benefits and Pensions Monitor explains how this two-pronged advantage works, along with other questions about this benefit.

For instance, how do employee stock purchase programs work? And more importantly, is it really worth your company's time to set up a stock purchase program for employees? Read on and let’s get into it.

The basics of stock purchasing plans for employees

An employee stock purchase program (ESPP), also known as an employee stock purchase plan, allows employees of a company to buy stock at a discounted price.

Under the program, an employee can purchase a certain number of shares in the company they work for at a price below the fair market value (FMV). Typically, these plans give a discount of up to 15% off the stock’s market price. The company can set the discount rate of their shares available to employees and can also limit the amount of shares an employee may buy.

Depending on the company, employees can have their stock purchase payments taken from automatic payroll deductions. The company can then use these funds to buy company stock on the employees’ behalf. These stocks represent the employees' financial share and partial ownership of the business.

An employee benefit like this would certainly appear enticing to potential hires, especially when packaged with the most popular employee benefits that Canadian employers offer.

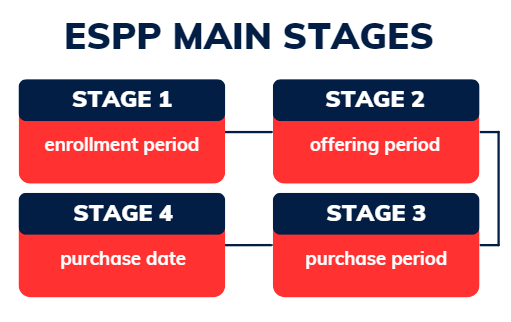

How an employee stock purchase program works

The ESPP is typically a process that involves four main stages. Here’s how the ESPP process works:

1. The enrollment period

This is the first step in the ESPP and it’s when employees decide to participate and enroll in the plan. Enrollment is voluntary. In most cases, the enrollment period of an ESPP occurs in the two to five weeks prior to the offering period.

After the enrollment period's close, employees may have to wait until the next offering period to participate if they are unable to enroll. It’s crucial for HR staff to issue memos informing employees of the enrollment period and have the plan document available for employees to review.

2. The offering period

Once an employee enrolls in the ESPP, they become eligible to participate in what’s called the offering period. For this period, employees can purchase company shares at a mutually agreed, discounted price. The discount often ranges from 5% to 15% less than the FMV of the shares on the open market.

The offering period can usually last for 12 months.

3. The purchase period

The following period is the purchase period. During this time, employees are informed of a series of purchase periods in which they can set aside funds for buying the shares. The purchase period often lasts for about 6 months.

4. The purchase date

This is when employees can make their official purchase of shares. The purchase date is often at the end of the purchase period. In an ESPP, the purchase date will depend on when the company sets them.

A purchase date also signals the end of the time allotted by the company to buy shares for participating employees. It is possible for companies to set several purchase periods. For instance, a company can set three purchase periods within an 18-month offering period.

Here’s a summary of the process for employee stock purchase programs:

The lookback feature

To make an ESPP more appealing for employees, a company has the option to offer a ‘’lookback” feature aside from the discount offered. Let's assume that ABC Company offers an ESPP, and the price of their shares is at $10 per share on the stock exchange. If they offered a 15% discount, then the share price for employees would be $8.50.

Assuming that on the purchase date, the stock price rose to $12. With the 15% discount, the share price would then be $10.20. With the lookback feature, the company would allow employees to buy at $8.50 a share, as it’s the lower price of the two. If there was no lookback feature, employees would only be able to buy at $10.20 a share.

So, the ESPP lookback feature lets employees purchase the share price of either:

- the initial date of the offering period or

- the purchase date

The lookback feature allows employees to pay the share price that is the lower of the two.

Typical employee eligibility requirements to purchase stock

In general, most employees are eligible to participate in the employee stock purchase program. However, the plan document can have some eligibility requirements. These requirements can vary from company to company. Some examples are:

-

vesting period – some companies may require that an employee be with the company for at least a year before participating in the ESPP

-

stock purchase limit – there can be restrictions on employees who have acquired some company stock through the ESPP. Typically, employees who already possess 5% of the company’s stock may be barred from purchasing any more stock.

Types of employee stock purchase programs

In general, there are two types of ESPPs used:

Qualified plans

Employers that offer this type of ESPP follow strict rules and guidelines on tax compliance. Employees who partake in the plan can buy shares at a discount. In qualified ESPPs, the share price is less than the fair market value (FMV) and employees need not pay taxes on the shares they purchase.

Qualified ESPPs must have the approval of the company’s shareholders within a year of implementation.

Those who participate in a qualified ESPP often have equal rights, with the offering period being for less than 3 years. During the offering period, the company accumulates payroll deductions to purchase stock in the ESPP.

Usually, there are restrictions on the maximum discount price a company can offer. Employees who take part in a qualified ESPP can get great tax benefits. The government doesn't recognize the discount as taxable income until they sell their stock.

When employees sell their stock, the difference between the discounted rate and the current fair market value (i.e., the profit if the FMV is greater than the discounted share price) becomes part of their taxable income.

Non-qualified plans

As for non-qualified ESPPs, these offer more flexibility as they are subject to fewer regulatory requirements. This translates to the absence of price restrictions and no requirement for any shareholders’ approval.

Employees do not enjoy any tax benefits under this type of ESPP. As with qualified ESPPs, the government taxes the difference between the discounted price and the fair market value, treating it as ordinary income when employees buy shares.

Does your employee stock purchase plan have a mandatory holding period?

— T.J. van Gerven, CFP® (@TJvanGerven) April 13, 2024

While this seems to be less common, when an ESPP has a holding period requirement, it changes the potential benefit of any discount or lookback pic.twitter.com/qclFyIN7Tl

Looking for more detailed advice on employee stock purchase programs? Visit our Best in Pensions and Benefits page for the top experts and consultants in the field.

How employees pay taxes on an employee stock purchase program

How the employee stock purchase program is taxed in Canada depends on whether it is a qualified or non-qualified ESPP.

Taxes on qualified ESPP

There are two types of sales for qualified ESPPs:

-

qualifying disposition (QD) – this type of sale is where shares are held over 1 year after the purchase date and over 2 years after the offering date

-

disqualifying disposition (DD) – this type of sale is where shares are held for less than 1 year after the purchase date or less than 2 years after the offering date

In either case, no tax is chargeable at purchase, but ordinary income tax and capital gains tax are applied at the time of the sale.

If the sale is a QD, the gains are considered long-term capital gains where the tax rate is lower than ordinary income. If it’s a DD sale, then the gains are considered short-term and are taxed at a higher rate.

Taxes on non-qualified ESPP

Non-qualified ESPPs have simpler tax rules. Income tax is applied only at the time of the purchase of the shares. Also, income tax only applies on the difference from subtracting the purchase price from the FMV of the shares as of the purchase date. This difference is taxed as ordinary income.

Capital gains tax (whether capital gains or loss), meanwhile, are chargeable at the time of the sale of the shares. Capital gains tax is computed by subtracting the sale price from the FMV of the shares at the time of the sale.

What happens to an ESPP when an employee leaves?

In cases where an employee leaves the company after buying shares, they have the option to keep the shares. However, departing employees can no longer buy additional shares through the ESPP.

An employer can refund ESPP contributions to a departing employee if:

- the employer has not yet bought the shares for them

- the employee left before the purchase period

Another option is for the departing employee to sell back the shares to the company at fair market value.

Should your company really set up a stock purchasing program?

The employee stock purchase program has several benefits, both for employers and employees alike. But is it truly a viable option for enhancing an organization’s employee benefits package? Here’s what we know:

For employers, the ESPP can help them attract and retain high-performing employees. The ESPP can potentially reduce younger workers’ anxiety about their financial future. An employee who invests in company shares (and derives financial benefits from them) is more likely to stay with the company for the long term.

As for the employees, they can use the ESPP to earn more money apart from their salaries or other investments and build their retirement nest egg. This is made possible through buying company shares at a discounted price, and having the lookback feature that reduces the price of the shares even more. Additionally, if the company’s stock performs well and increases in value over time, then employees who own shares will see even greater gains.

If all these ESPP elements work out, the prospect of “free money” for the employee participants is virtually guaranteed.

The ESPP is an excellent benefit that employees should take advantage of. Here's a video that offers some helpful suggestions on how your employees can flip those shares into other investments. Investing exclusively in company shares is not the best strategy.

Employers and HR staff who wish to see improved productivity must offer benefits that attract and keep top talent. The ESPP, along with other employee benefits, can be among the most unique and indispensable tools in your benefits repertoire.

Offering this employee benefit has its caveats, though. An ESPP means an increased workload for HR, accounting, and administrative departments. An internal communications plan is also crucial to convey this benefit to employees, ensuring they understand the benefit and it is executed without any hitches.

Properly leveraging the ESPP can indeed help you recruit the best talent and retain them. This can snowball into increased productivity, achieving company goals, and fostering a shared responsibility for both personal and company success.

Let us know what you think about the employee stock purchase program in the comments.