De-risking, pension risk transfers are strategies outlined by Normandin Beaudry

Normandin Beaudry’s latest Pension Plan Financial Position Index found that both going concern and solvency ratios have seen substantial improvements, putting plan sponsors in a position they haven’t experienced in years - deciding what to do with surpluses instead of how to manage shortfalls.

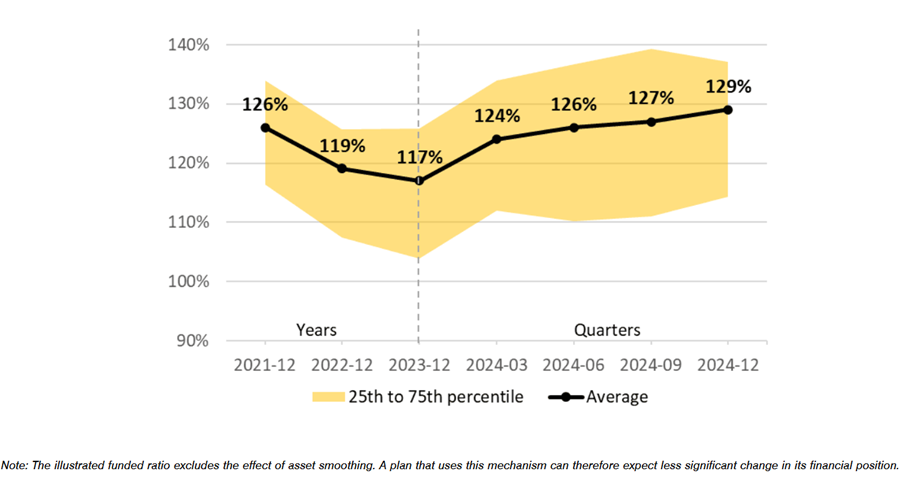

The Index results ultimately provide a promising future for pension funds as going concern numbers sit at 129 per cent with solvency ratios hovering at 114 per cent as at December 2024. This is a stark reversal from the deficit-ridden past that forced many sponsors to make difficult choices.

"We're in a situation where pension plans are in a very good financial position. I've seen financial crises, legislative changes, and relief measures introduced every few years to help struggling pension plans. But in the last two or three years, we’ve seen the complete flip side of the story,” highlighted Claude St-Laurent principal, pension and savings at Normandin Beaudry.

Historically, low interest rates from 2008 to 2022 inflated liabilities, leading to persistent funding shortfalls and forcing plan sponsors to focus on additional contributions and benefit reductions, explained Pierre-Luc Meunier, partner, pensions and savings at Normandin Beaudry.

However, with rising interest rates, liabilities have decreased. Today, approximately 80 per cent of pension plans are in a surplus position.

“Plan sponsors want to take some risk off the table but not all the risk because you have to take some risk to make returns,” said Meunier. “But a lot of plan sponsors say, ‘I have this surplus but I would like to save some for bad days so how do I make sure that there is some surplus that is still there when the storm comes?’”

Normandin Beaudry pointed to some strategies that can help with the long-term preservation of all these gains. One example is de-risking retirees’ money, while noting there are two ways to do that: within the portfolio itself, like shifting the asset mix to be more liability-driven, with a focus on matching assets and liabilities; or perform a pension-risk transfer through annuity purchases.

Courtesy of Normandin Beaudry

As Meunier noted, in 2024 alone, over $10 billion in pension liabilities were transferred to insurers in Canada, setting another record for the annuity market.

“These are the kind of moves that plan sponsors are doing right now to avoid the storms in the future,” he said.

Plan sponsors can also look to having an actuarial evaluation done because it's an accurate measure of the current situation, allowing sponsors to see “the current state of things,” noted Meunier.

Alternative assets like real estate and infrastructure are another consideration. Once considered niche investments, they have become a core part of pension fund portfolios.

"They’re no longer considered that alternative anymore, they've become a third pillar in investment policy," said St-Laurent. "Just about every pension plan today has some allocation to bonds, to equity, but also to real estate or infrastructure or both."

Additionally, conducting stress testing and scenario analysis to identify potential risks as well as enhancing cybersecurity measures to protect against data breaches and integrating ESG factors into the investment process are other preservation strategies Normandin Beaudry highlighted.

Governance is also coming under greater scrutiny, notably with the introduction of CAPSA Guideline No. 10, which outlines risk management expectations for pension plans. While the guideline is not technically a legal requirement, regulators have made it clear that compliance is expected.

"If a pension administrator does not follow those guidelines, it exposes them to quite a large amount of risk when it comes time to defend themselves in cases of possible litigation," St-Laurent noted.

Diversification remains the buzzword

Of course, the goal for any pension plan is also to choose a well-diversified investment policy. One major driver that’s attributed to pension surplus has been market performance as US equities have soared, particularly led by the Magnificent Seven.

"Five years ago, the seven largest U.S. stocks made up 12 per cent of the global index. Today, they account for 24 per cent,” noted St-Laurent.

While the growth has been a windfall for pension funds, it also raises concerns about concentration risk and the sustainability of returns.

“Active management has been a little difficult for managers who've tried to have a more diversified approach, who maybe under weighted these companies and maybe subtracted a little better bit of value,” St-Laurent noted.

“Being conscious of that risk and certain strategies in active management can allow a better diversification of assets,” he explained. “That might be an important step that pension plans could take in order to maintain the gains that have been realized over the last several years.”

Despite the strong numbers in growth, plan sponsors are encouraged to tread carefully. The 1990s saw a similar surplus situation, but the response was vastly different.

Back then, pension managers used excess funds to encourage early retirements, creating room for younger employees to enter the workforce. That approach doesn’t quite fit in today’s labour market.

"The thinking is quite different," Meunier said. "We don’t want to encourage earlier retirement. We’re trying to find ways to keep and attract employees to give us a few extra years."