Learn all about Quebec pension plans, including the QPP, employer options, and private savings strategies. Plan your retirement with confidence. Start today

If you’re working in Québec and your income meets the minimum threshold, you and your employers are required to contribute to the Québec Pension Plan (QPP). The QPP is the Canada Pension Plan’s (CPP) counterpart in the province. It is designed to provide you and your family with financial protection upon retirement or in cases of disability or death.

The QPP, however, is just one of the several pension plans Québec employees can access.

In this article, Benefits and Pensions Monitor gives you an overview of the different retirement schemes available in the province. We will touch on relevant topics, including eligibility requirements, contribution rates, and features and benefits.

If you have questions about the Québec Pension Plan and your other options for retirement income, this guide can be a useful resource. Keep reading as we discuss the different ways you can achieve financial security upon retirement.

What is the Québec Pension Plan?

When the federal government proposed the Canada Pension Plan in the mid-1960s, Québec opted out and set up its own pension scheme, the Québec Pension Plan. Just like the CPP, the QPP serves as a mandatory public insurance plan for workers in the province. It provides employees and their families with retirement income, and disability and death benefits.

The funds from the QPP come from payroll contributions from employees and their employers. Retraite Québec is in-charge of the administration, while Caisse de dépôt et placement du Québec (CDPQ) serves as the fund manager.

Learn more about the similarities and differences between the QPP and CPP in this guide to Canada Pension Plans.

How does the Québec Pension Plan work?

Here are the essential aspects of the Québec Pension Plan that you need to take note of:

QPP eligibility requirements

If you’re part of Quebec’s labour force, then you’re required to contribute to the QPP if you meet these criteria:

- you’re at least 18 years old

- your annual income exceeds $3,500

QPP contribution rates

The QPP consists of two parts: the base plan and the additional plan, which was introduced in 2019. The latter serves two purposes:

- It increases the rate at which income is replaced from 25% to 33.33%

- It raises the earnings cap to 114% of the maximum pensionable earnings (MPE)

If you’re a salaried worker, your employer is required to contribute as much as you. For 2025, the contribution rate remains at 6.4% – 5.4% for the base plan plus 1% for the additional plan – for a total of 12.8%. If you’re self-employed, you will need to cover both parts of the contribution.

The rate, however, applies only if you’re earning between the basic exemption amount of $3,500 and the MPE of $71,300. Salaries exceeding this amount up to $81,200 are subject to a 4% contribution rate – a total of 8%, including that of employers – for the additional plan. You’re no longer required to contribute for earnings above $81,200.

You can find the complete benefit amounts and key data for the Québec Pension Plan on this webpage.

QPP benefits

You and your family are eligible for various pensions and benefits depending on how much you’ve contributed to the plan. Here’s how these benefits work:

Retirement income

Your pension is calculated based on your earnings since you turned 18. The amount you will receive each month depends on when you retire. You will get 100% of the pension’s value if you retire at age 65. This is the normal retirement age under the Québec Pension Plan.

You can receive a higher amount, however, if you hold off on retirement. Your retirement payout reaches its maximum when you turn 72. On the flipside, retiring before turning 65 reduces your monthly pension.

Disability benefits

To receive disability benefits under the QPP, you must:

- be under age 65

- unable to work or your income has decreased considerably due to your health condition

- earn less than $1,728 gross (before taxes) per month

- be deemed to be disabled by Retraite Québec’s medical advisors

- have sufficiently contributed to the QPP

- not be entitled to an unreduced income replacement indemnity from the Commission des normes, de l'équité, de la santé et de la sécurité du travail (CNESST)

- not be receiving a retirement pension under the CPP

If you’re under 60, you will receive a monthly disability pension of $583.29 – which is the same for all beneficiaries – and an amount calculated based on your earnings filed in the QPP. If you’re between 60 and 65, you will receive your monthly pension in addition to the disability payout.

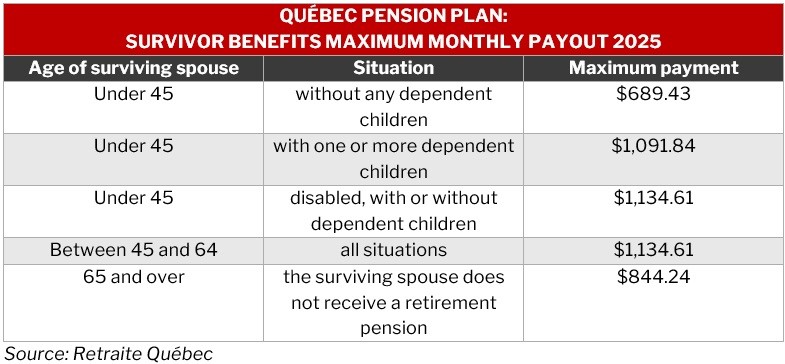

Survivor’s benefits

The QPP ensures that your spouse or common law partner receives a basic income after your death. The monthly payouts will depend on a range of factors, including:

- the contributions entered in your spouse's file under the QPP and CPP

- your retirement pension supplement

- your age

- whether your spouse supports your dependent children

- whether you were deemed to be disabled by Retraite Québec

- whether you were receiving retirement or a disability pension under the QPP or CPP

The table below lists the maximum payout your spouse or common law partner can receive under the Québec Pension Plan’s survivor benefits.

Orphan’s pension

Any of your children under age 18 are eligible for orphan’s pension under the QPP. They can be your biological or adopted children living with you for at least a year before your death. The maximum orphan’s pension is set at $301.77 per month in 2025. The amount is payable to the person who will be providing for your child.

Death benefit

A maximum death benefit of $2,500 can be given to any person or charitable organization who paid for your funeral expenses. To claim, they must provide proof of payment to Retraite Québec.

Some funeral expenses that can be reimbursed include:

- transportation, storage, and preservation of the body

- embalming of the body

- interment, cremation, or aquamation

- coffin

- urn, funeral jewellery, reliquaries, tree of life

- visitation at the funeral home

- funeral service

- publication of death notices

- services of a funeral director

- cemetery plot, niche and funerary recess

- funerary monument or inscription

- acknowledgement cards, memorial bookmarks

- taxes related to eligible expenses

Flowers and reception services aren’t reimbursable items under the Québec Pension Plan’s death benefit.

What other pension plans can you access in Québec?

Apart from the QPP, there are several other schemes that you can take advantage of to build your retirement income while working in the province. These include:

1. Voluntary retirement savings plan (VRSP)

The voluntary retirement savings plan is a type of defined contribution pension plan designed for workers in Québec without access to a group pension plan. It functions almost exactly like a pooled registered pension plan (PRPP) offered in other provinces.

The VRSP was created to ensure that all employees in the province have access to a group savings plan. The plan serves as a straightforward and more affordable alternative to traditional workplace pension.

Québec employers with at least five workers are legally required to provide their staff with a VRSP. If your employer offers one, you’re automatically enrolled as long as:

- you’re at least 18 years old

- you have a year of uninterrupted service within the company

Your employer is responsible for notifying you of your enrollment. This must be done at least 30 days before implementation. After that, you have 60 days to opt out. Staff members who didn’t qualify but wish to participate may do so by informing the employer of their intention.

If you choose to participate in the VRSP, you must contribute a portion of your paycheque, just like in a group registered retirement savings plan. By default, contributions are set at 4% of your gross salary. Your contributions are also not subject to payroll taxes, unlike those in a registered retirement savings plan (RRSP).

Employers, on the other hand, aren’t required to make VRSP contributions. You can learn more about how voluntary retirement savings plans work in this guide.

2. Locked-in retirement account (LIRA)

A locked-in retirement account is a special type of registered retirement savings plan (RRSP) where you can transfer funds from your VRSP and other supplemental pension plans. But unlike a traditional RRSP, the funds in LIRA are locked in as they are intended to provide income in your retirement.

You can only start withdrawing from your locked-in account once you reach age 65 on December 31 of the previous year. On the flipside, you can only hold a LIRA until 31 December of the year you reach age 71.

3. Life income fund (LIF)

A life income fund is a type of registered retirement income fund (RRIF) where you can transfer money from your VRSP, LIRA, and other supplemental pension plans. The funds transferred to your LIF grow tax-free until withdrawal and provide you with a source of retirement income.

As part of the 2025 changes, Québec has removed the maximum withdrawal limit from the LIF. The goal is to give fund holders more flexibility on how much retirement income they receive. This means that once you turn age 55, you can withdraw the entire amount of your life income fund.

Previously, LIF withdrawals were subject to minimum and maximum limits, just like in other jurisdictions.

4. Public-sector pension plans

Public-sector pension plans are designed for employees in the public and parapublic sectors in Québec. These include the public service, education, healthcare, and social services sectors.

If you’re working in the province’s public sector, these are some of the pension plans you can access:

- Government and Public Employees Retirement Plan (RREGOP)

- Pension Plan of Management Personnel (PPMP)

- Retirement Plan for Senior Officials (RPSO)

- Pension Plan of Certain Teachers (PPCT)

- Teachers Pension Plan (TPP)

- Civil Service Superannuation Plan (CSSP)

- Pension Plan of Peace Officers in Correctional Services (PPPOCS)

- Pension Plan for Federal Employees Transferred to Employment with the Gouvernement du Québec (PPFEQ)

- Retirement Plan for Active Members of the Centre hospitalier Côte-des-Neiges (RPCHCN)

- Pension Plan of Elected Municipal Officers (PPEMO)

- Pension Plan of Certain Judges Appointed before 1 January 2001 (PPCJBJ)

- Pension Plan of Certain Judges of Québec (Part V.1 of the Courts of Justice Act) (PPCJQ)

- Pension Plan of the Members of the National Assembly (PPMNA)

- Superannuation Plan for the Members of the Sûreté du Québec (SPMSQ)

All public-sector pension plans in the province are administered by Retraite Québec.

5. Private pension plans

Private pension plans are designed to supplement the retirement income you will receive from public pension plans. There are several types of private plans, which include employer-sponsored plans and RRSPs.

Here are some common examples:

Supplemental pension plan (SPP)

In this type of plan, your employer makes contributions to provide you with retirement income and other benefits. Depending on the terms of the contract, you may or may not need to contribute to the plan. The funds in an SSP are frozen and can only be used in retirement.

Excess benefit plan

Also referred to as top-hat plan, this is designed to supplement SPP retirement income without regard to tax limits. The plan is often suited for high-income and key employees.

Group registered retirement savings plan

A group RRSP serves as a savings and investment program set up by your employer to help you save for retirement. Contributions are deducted automatically from your paycheque.

Group registered retirement savings plans function mostly like individual RRSPs. The main difference is that group RRSPs are managed by your employer, who has the option to match your contributions.

Deferred profit-sharing plan (DPSP)

This is where employers share a part of their profits with employees. Contributions are determined based on the company's profits.

Only employers contribute to a DPSP. The funds built up may be paid out either in a lump sum or in multiple instalments over a period not exceeding 10 years. These can be used to buy annuities from an insurer. They can also be transferred to an RRSP or SPP.

Employees profit sharing plan (EPSP)

Another plan where employers share a portion of their profits with employees. But unlike in a DPSP, employees can contribute and must pay taxes on the contributions made on their behalf, even if they don’t withdraw the benefits.

Retirement compensation arrangement

In this arrangement, the employer, and sometimes the employee, pays into a trust or other fund. The goal is to provide you with a retirement income if you lose your job or your job duties change radically.

Check out our list of the 10 best pension plans in Canada for more information on how you can build your retirement savings.

Did you find this guide on Québec pension plans helpful? Let us know in the comments.