Colin Ripsman provides an investment outlook on what pension funds should expect for the year ahead

Economic Growth Outlook

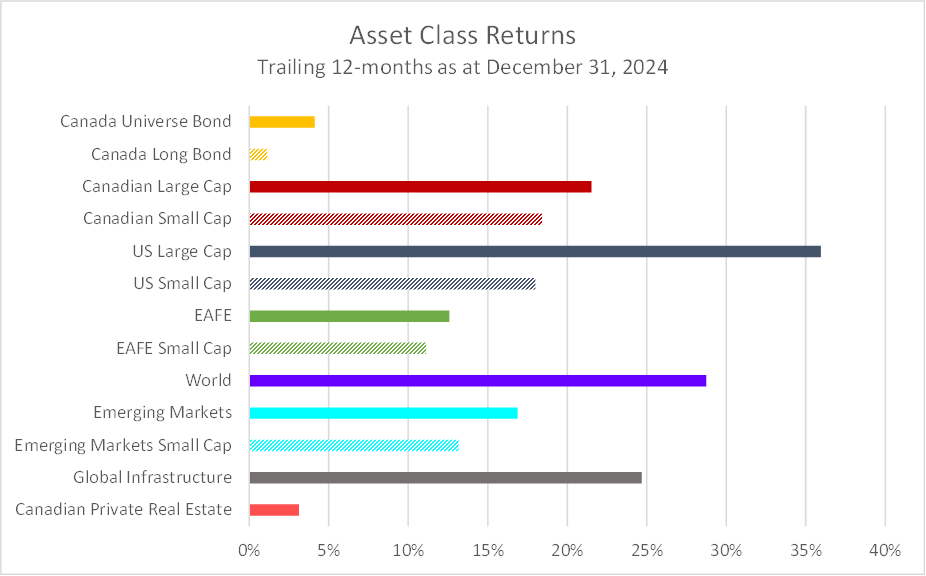

2024 was an outstanding year for pension funds, with the median global balanced portfolio returning 17% over the 12-month period ending in Q4 2024. This strong performance benefitted pension funds across regions. Large-cap developed market equity returns varied, ranging from a low of 13% (EAFE) to a high of 36% (US), with Canadian equities returning 22%. Large-cap equities notably outperformed small-cap stocks, and developed markets outperformed emerging markets, which gained 17%. Fixed income also had a reasonable year, with Canadian universe bonds returning 4%, as interest rates began to decline mid-year, particularly at the shorter end of the yield curve. However, real estate struggled, with the median Canadian private real estate fund returning 3%, reflecting the ongoing recalibration of valuations in sectors such as office and retail, which continue to adjust to post-COVID demand patterns.

Exhibit 1 – Index Returns

Looking ahead to 2025, we expect mixed performance across regions and asset classes, as several significant headwinds may affect global markets. Equity returns are forecasted to range from 4% to 11%, depending on the region. Bond portfolios should benefit from falling interest rates, as central banks continue to cut rates in response to a softening economic environment. We anticipate continued strength in US equities, driven by a resilient US economy and investor enthusiasm for artificial intelligence. Conversely, Canadian, European, and emerging market equities are expected to face challenges, particularly as the new US administration signals an intention to raise tariffs, which could disrupt global trade and supply chains.

Economic Growth

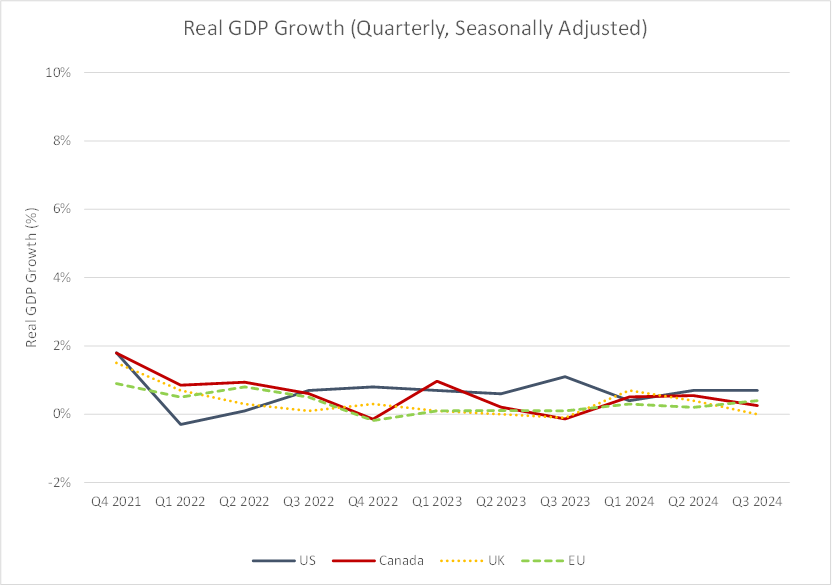

Global economic growth is expected to slow in 2025, partly due to ongoing geopolitical instability in Europe and the Middle East. Additionally, signals from the new US administration suggest the potential imposition of new trade tariffs on several countries and regions, including China, Canada, Mexico, and the European Union. If these tariffs are implemented, they could severely curb economic growth in these regions, given the size and importance of the US market. The US may also face countervailing tariffs on its exports, which could further dampen domestic growth.

In Canada, slower or even negative economic growth is likely, as reduced trade and global economic slowdowns will weigh on demand for commodities. We also expect consumer spending to decelerate, due to rising unemployment and mortgages renewing at higher rates. US GDP is expected to show modest growth in 2025, while growth in Europe and the UK is likely to remain weak due to continued disruptions from the Ukraine conflict, ongoing Middle East instability, and political upheaval in major European economies. Central bank rate cuts should provide some relief, helping to partially offset these negative factors.

Exhibit 2 – GDP Growth

Fixed Income

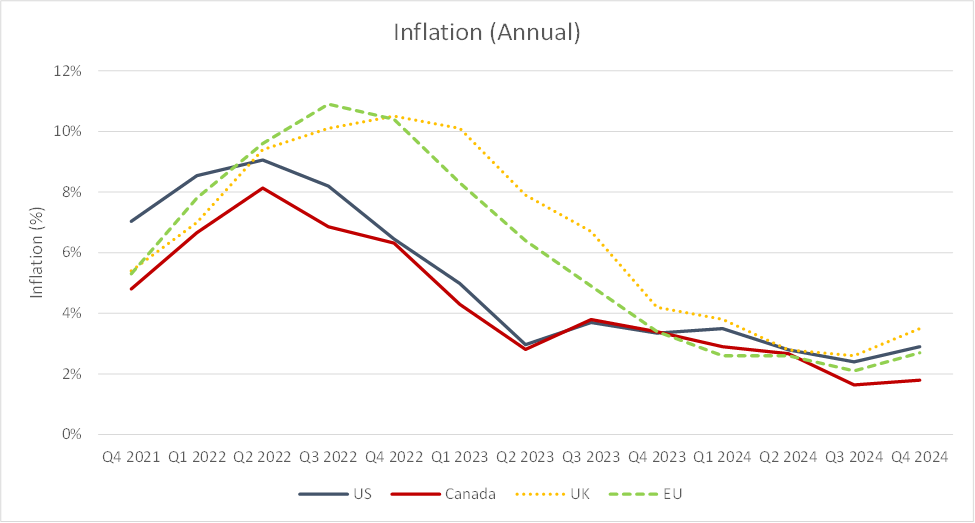

In 2024, central banks in developed markets began cutting interest rates as inflation eased. We expect further rate reductions in 2025, as central banks strive to stimulate economic growth. Inflation in both Canada and the US peaked in mid-2022 (see Exhibit 3) and has been steadily declining since then. Canadian inflation fell below the Bank of Canada's long-term target of 2% in Q3 2024.

Exhibit 3 – Inflation

Given reasonable current yields and the expected continuation of interest rate cuts in 2025, we anticipate strong performance for Canadian fixed income portfolios. Should mid-term rates decrease by 0.5%, we forecast returns of 6-7%. A prolonged economic slowdown could widen corporate bond spreads, resulting in them potentially underperforming government bonds.

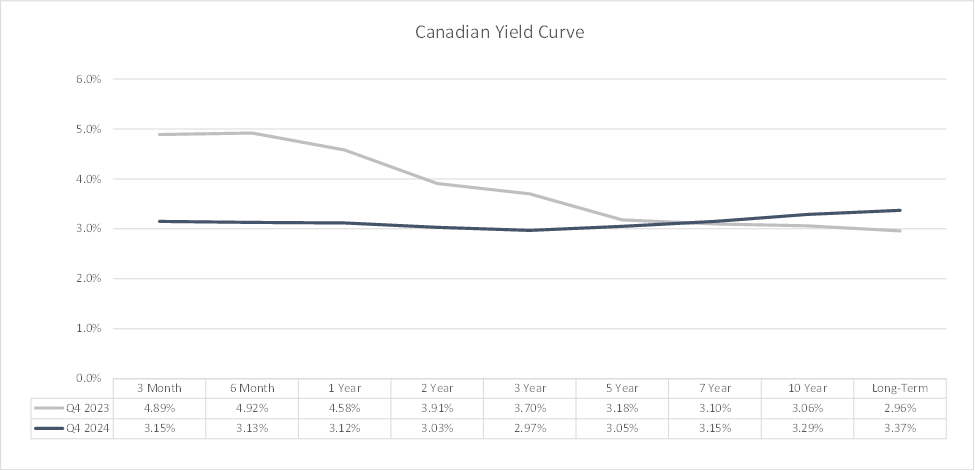

The Canadian yield curve flattened during 2024 (Exhibit 4), reversing its inversion. In 2025, we expect short-term rates to continue falling, leading to a more traditional upward sloping yield curve. As a result, we expect universe bonds to marginally outperform long bonds.

Inflation levels in the EU and the UK peaked in early 2023 and are currently running higher than in Canada but are still at reasonable levels; 2.7% in the EU and 3.5% in the UK. This provides both the EU and UK central banks some room to further reduce interest rates in 2025 to stimulate their economies.

Exhibit 4 – Canadian Yield Curve

Equities

In Canada, we anticipate a more challenging equity market in 2025, driven by weaker GDP growth, declining consumer spending, and higher unemployment levels. We expect sluggish global economic growth to dampen demand and exert downward pressure on commodity prices, which will likely impact the energy and materials sectors—two significant drivers of the Canadian market. Additionally, new or increased tariffs from the US could further slow economic growth both locally and globally.

However, interest rate cuts may alleviate some of the debt burden on Canadian consumers and improve corporate earnings. As a result, we expect Canadian equities to return 4-6% in 2025.

In the US, we expect moderate economic growth and an avoidance of a recession. Strong US economic performance, particularly in technology sector, should drive continued equity growth, with our expected returns in the 9% to 11% range. Investors looking to shelter their portfolios from global uncertainties should consider increasing allocations to US equities.

UK equities are expected to underperform US equities, as higher inflation and slowing consumer spending weigh on economic activity. Meanwhile, lower inflation in the EU should support moderately better European GDP growth relative to the UK. We expect European equities to outperform UK equities and range from 6% to 8%.

The ongoing Russia-Ukraine conflict will continue to create economic challenges in Europe, dampening earnings for companies operating in the region. Overall, we foresee a slowdown in global economic growth, leading to lower corporate earnings, especially in growth-oriented sectors like technology, which may underperform relative to value stocks.

Small and mid-cap equities may see some benefit from increased buyout private equity fund activity, and corporate acquisitions, spurred by lower interest rates.

Alternatives

Canadian real estate is expected to see a modest recovery in 2025, with returns in the mid-single-digit range, as property valuations have already adjusted downwards in 2024. Recent interest rate cuts should help support property values. Infrastructure investments are also projected to perform well, benefiting from ongoing infrastructure spending and lower borrowing costs.

Despite their higher yields, mortgage funds are expected to underperform bond funds in a falling interest rate environment, due to their shorter relative durations.

We expect to see higher private equity returns in 2025 as a consequence of lower interest rates, which should lead to lower financing rates, and higher company valuations. A lower interest rate environment should also lead to increased deal activity in buyout-focused private equity funds.

Capital Market Assumptions

The following table reflects our capital market expectations for 2025:

Exhibit 5 – Capital Market Projections – 2025

|

Asset Class |

Return Projection |

|---|---|

|

Canadian Universe Bonds |

6-7 percent |

|

Canadian Long Bonds |

8-10 percent |

|

Canadian Equities |

4-6 percent |

|

US Equities |

9-11 percent |

|

International Equities |

6-8 percent |

|

Canadian Real Estate |

4-6 percent |

|

Infrastructure |

7-9 percent |

|

Canadian Mortgages |

5-6 percent |

|

Balanced Portfolio1 |

6-7 percent |

1Comprised of 40 percent Canadian Bonds, 20 percent Can Eq, 20 percent US Eq, 20 percent International Equity

Colin Ripsman is the Founder and President of Elegant Investment Solutions, inc., a boutique investment consulting firm that supports DC and DB plan. Colin has 30 years of experience in the investment industry, where he held leadership roles with several leading consulting and investment management firms.